What Are Kids Going To Do?

Every time I see new innovation come our way; I can't help but think 'What are my kids going to do!?” Their future depends on the ability to adapt to fast-moving trends, to be prepared for a world that looks much different than today's. Education may be their best chance!

You can't go through a day lately without hearing the words 'Artificial Intelligence'. It’s coming fast and will have an impact on all of us, both positively & negatively. It's allowing us to be more efficient than ever but if we're not prepared to evolve it can work against us. If you haven't seen the 60 Minutes piece on AI (Artificial Intelligence) with Google CEO Sundar Pichai, I highly recommend you watch it immediately! In 2017, I wrote a college planning email called 'Debt & Robots - A College Graduates Challenge'. The story still holds true, only it's happening quicker.

Artificial Intelligence - 60 Minutes

Debt & Robots - A College Graduate's Challenge - Hamilton Wealth

As it always does, the world will change and evolve, though seemingly faster every year. I can't help but think of my past as new innovations become a part of our daily lives. The children's tv show, The Jetsons, was created in 1962, an animated series that showcases several futuristic ideas that we use today. A live-in robot (Rosie) handles most daily functions for the family. You'll see automatic vacuums, digital newspapers, video calls/meetings, and even a smart watch used to communicate. Again, this was created in 1962, over 60 years ago! The Jetson family also got from place to place in a flying car (to be determined). Many other movies and shows also used technologies we thought were crazy at the time but are very relevant today: The Terminator (robots and drones), RoboCop (facial recognition, robots), Contagion and Outbreak (pandemics), War Games (hackers) just to name a few.

The jobs market will look very different in the next 10-20 years than it looks today. The same held true for those searching for jobs in the previous 10-, 20-, and 30-years ago. Just ask parents or grandparents what they did in the past. Think of the auto industry, coal industry, and newspaper business. These were highly sought after jobs by Americans in the past. These industries look very different today due to advances in technology and automation, some will become obsolete if they aren't already. Products come and go and so will jobs. These are products that have become obsolete in most homes, due to innovation: typewriters, 8 tracks, encyclopedias, paper maps, walkman, phonebooks, floppy disks, pagers, phone booths, ipods!. There are also jobs that have vanished and rapidly declined because of innovation and technological advances. Salesmen used to go door to door selling vacuums and encyclopedias. Milkmen used to deliver milk to our doorsteps! The mining (coal) industry, agriculture industry, and manufacturing jobs have been severely impacted and declining for decades. Tractors reduced the need for farmers, alternative energy is replacing coal, and cheap labor (overseas) and automation is replacing factory workers. These changes have made food and products cheaper, allowing for more consumer spending on things like food, travel, health care, and education. Conversely, industries like healthcare, retail, education, and technology have increased over the last several decades. The share of white collar and service jobs have increased while blue collar jobs and farming have decreased significantly. The chart below displays a simple breakdown of employment history since 1850. In 1850, farming accounted for 51% of the jobs, whereas today it is approximately 1% of jobs.

Nine Things That Have Become Obsolete In The Last 20 Years - Business Insider

Obsolete Technologies That Will Baffle Modern Generations

Goldman Sachs predicts 300 million jobs in the world, including two-thirds of jobs in the US and Europe are at risk due to AI (Artificial Intelligence). In the US, they predict 46% of office and administrative support could be replaced by AI. About 44% of legal positions could be automated and 37% of engineering jobs are at risk. Again, what exactly will our kids do for a living?

Goldman Sachs Predicts 300 Million Jobs Will Be Lost Or Degraded By AI

AI Could Replace Equivalent Of 300 Million Jobs

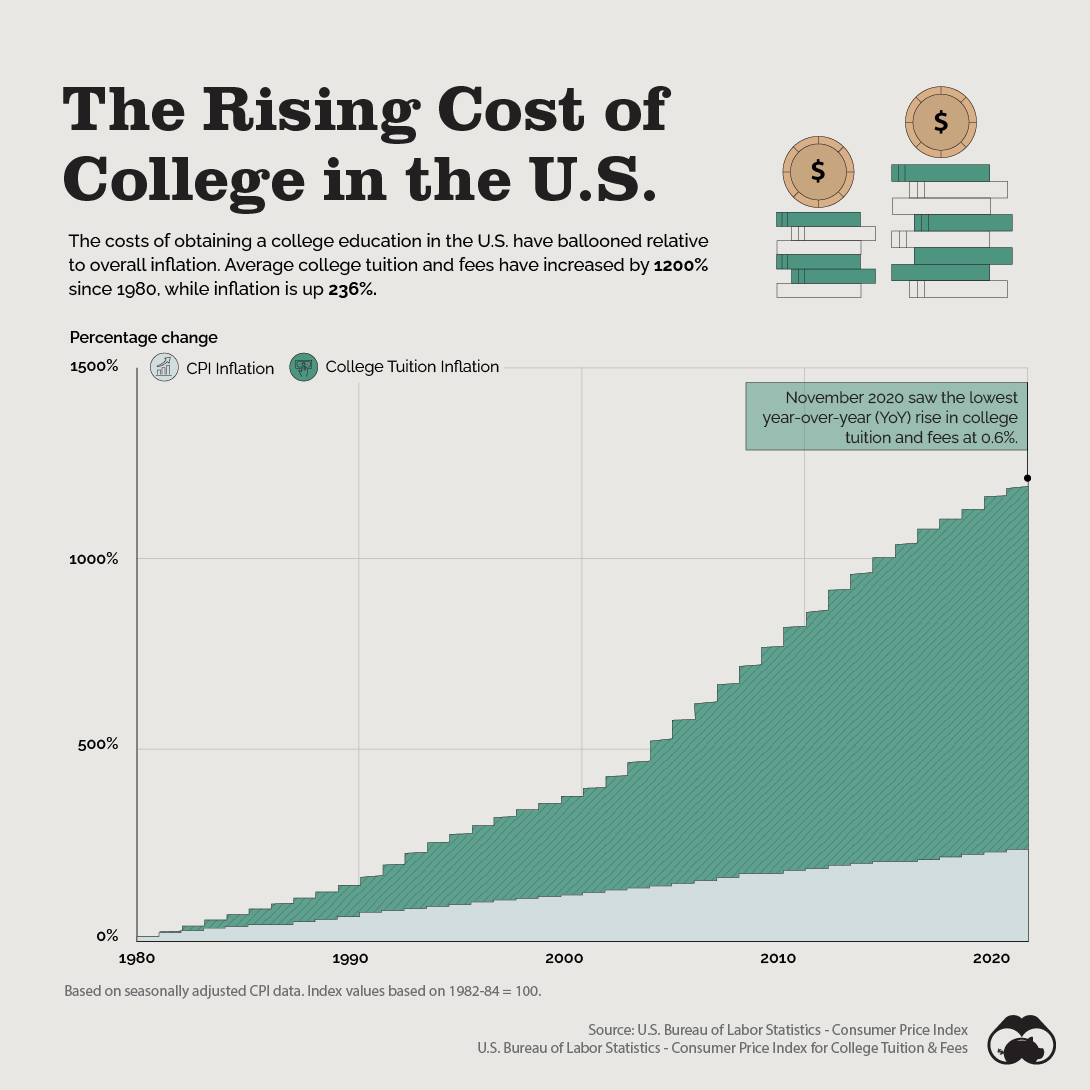

Educating kids for the future comes at a steep price, in money and effort. A child beginning college today will spend approximately $115K for a public university and $234K for a private university, tuition including room and board for four years. For a child born today attending college in 18 years, the cost will be $195K for a 4-year public university and $400K for a private university. These are national averages and will vary based on the university. For example, USC is much higher at $83K per year today or $347K in total ($590K total for a child born today). To make things even tougher, the acceptance rate at most colleges is much lower than it was years ago. For example, the acceptance rate at UCLA in California was 22% in 2013, it is 11% today. The competition is incredible, the amount of applicants to UCLA has doubled , at nearly 140K applicants today vs 72K in 2013.

A common objection we hear about investing in a college savings plan is the unknown of whether a child will need it. They may decide not to pursue college to start a business. They may earn a scholarship. They may attend a less expensive university, leaving unused funds in the college savings plan. Fortunately, legislation over the past several years makes the 529B college savings plan more flexible. Today 529B funds can now be used for precollege education and even retirement contributions.

The funds in a 529 college savings plan can be used for purposes other than college. They can be used for K-12 private education, up to $10K per calendar year.

There's a new benefit to save in a 529 College Savings Plan: retirement savings. The Secure Act 2.0 signed into law in Dec 2022 allows for excess funds in a 529 college savings plan to be moved into a Roth IRA for the child, beginning in 2024. This is a huge benefit that provides the child with a great head start towards retirement savings. There are some guidelines to be allowed to do this. The most important are that the 529 must be in place for 15 years (so don't wait!) and the contributions must be in the plan for five years, anything less will make the funds ineligible to move into a Roth IRA. Remember, a Roth IRA is a retirement account that grows tax deferred and comes out tax free when withdrawn, even the earnings.

I ran a simple illustration on what the numbers look like long term if converting unused 529 funds to a Roth IRA. I assumed a $7K annual contribution for 5 years ($35K total) beginning at age 22, post college. This is the max legislation will allow you to convert. We used a 7% return based on a balanced portfolio. At age 60, the Roth IRA (retirement account) value would be $408K. Of the $408K balance, $373K comes from the investment growth over 38 years. I don't think any child would be upset about the chance to accumulate this retirement balance before contributing any of their money for retirement (after college of course).

You Can Roll Your 529 Plan To A Roth IRA - Forbes

Remember, the benefits of 529 college savings accounts are that the funds grow tax deferred over time and are withdrawn tax free for qualified education expenses. Anybody can contribute to a 529 and they can be a great gift to not only kids but grandkids, nieces, nephews, or close friends.

As a Certified Financial Planner (CFP), it is my job to help you plan.

We are happy to run college projections at any time and for any college you'd like. We help establish 529B college savings plans for clients and we do not bill on these accounts. Click the button below and we’ll run your numbers and discuss the results with you.

Lets prepare the next generation for a future that seems increasingly, less certain.

Let us know if you have any questions.

Thank you,

Jerry

The opinions expressed in this communication are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. Any past performance discussed during this communication is no guarantee of future results. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Advisory services are only offered to clients or prospective clients where Hamilton Wealth, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Hamilton Wealth, LLC unless a client service agreement is in place.